The Excise & Taxation Commissioner, Haryana, Panchkula, on March 22, issued a clarification in the case of M/s Jasch Plastics India Ltd., Kundli, Sonepat. The company had sought clarification under section 56(3) of the Haryana Value Added Tax Act, 2003 on the following question:

“Whether, the non woven fabric is tax free under entry 51 of Schedule B of Haryana Value Added Tax Act?”.

The main extracts from this clarification are produced here for the general information.

The applicant – Jasch Plastics India Ltd. – is a manufacturer of non-woven fabric. The applicant states that non -woven fabrics are tax-free as per order of assessing authority, Bhiwani but another view may be expressed by assessing authority, Sonepat, therefore, a clarification is sought to know the correct liability of tax. Non-woven fabric, also known as ‘technical textile’, is used in manufacturing of air-filters for automobiles, surgical disposal caps, masks, vacuum cleaner bags, carry bags, for inner lining of suits, padding of shoulders etc. The applicant claims that ‘non woven fabric’ is a variely of textile and tax free under entry 51 of Schedule B. The applicant has relied upon the judgement of Supreme Court passed in the case of M/s Porritts and Spencer (Asia) Ltd. Vs. State of Haryana (1978 42-STC-433). The applicant has also relied upon the judgement of Supreme Court in the case of Delhi Cloth and General Mills Company Limited Vs. State of Rajasthan (1980) 46- STC-256 (SC), wherein the Court held that “fabric covers all textiles no matter how constructed”.

The matter has been examined. The applicant has claimed that the product, “non woven fabric” is covered by entry 51 of Schedule B and, therefore, is exempted from levy of VAT. For ready reference, entry 51 is reproduced as under:

“All varieties of cotton, woollen or silken textiles including rayon, artificial silk or nylon but not including such carpets, druggets, woollen durrees, cotton floor durrees, rugs and all varieties of dryer felts on which additional Excise Duty in lieu of sales tax is not levied.”

Perusal of the above entry reveals that only ‘textiles’ fall within the purview of this entry. The word ‘textile’ is derived from Latin word ‘texere’ which means ‘to weave’. When yarn, whether cotton, woollen, silken, rayon, nylon or of any other description is woven into fabric, what comes into being is a ‘textile’. The method of weaving adopted may be the warp and weft pattern which involves interlacing a set of longer threads (called the warp) with a set of crossing threads (called the weft). This is done on a frame or machine known as a loom. With the advent of science and technology there may be various processes or techniques of weaving. Whatever be the mode of weaving employed, woven fabric would be ‘textiles’. Fabric, on the other hand, is manufactured through weaving,knitting, spreading, crocheting, or bonding. Thus, ‘fabric’ is a wider term which includes woven fabrics (textiles) and also includes non woven fabrics, but the term ‘textile’ is restrictive which includes woven fabrics only.

As per Wikipedia,

“Nonwoven fabric is a fabric-like material made from lonq fibres, bonded together by chemical, mechanical, heat or solvent treatment. The term is used in the textile manufacturinq industry to denote fabrics, such as felt, which are neither woven nor knitted. Some nonwoven materials lack sufficient strenqth unless densified or reinforced by a backing. In recent years, nonwovens have become an alternative to polyurethane foam”

Non woven fabric is manufactured from Polypropylene Granules by adopting ‘Spunbond technology’. In this technique PP Granules are fed to the Hopper and at a certain temperature they are pressed through the extruder and melted. The molten polymer is filtered and passed through spinning unit and directly converted to numerous filaments called Polypropylene filaments. The filaments are laid in the form of continuous web on a conveyor belt. Under controlled pressure, thermal bonding of filaments eventually results into formation of non woven fabric.

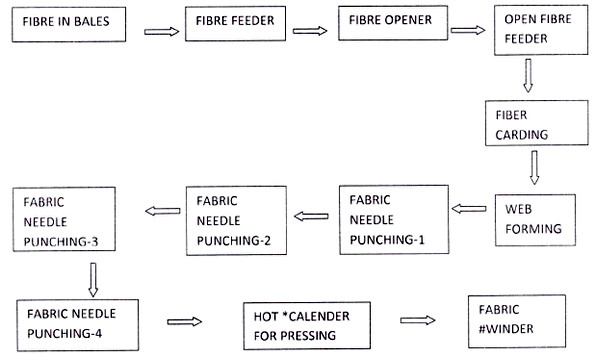

The flow chart for manufacturing of non woven fabric as obtained from the applicant is shown in Figure1. The flow chart reveals that neither yarn is used as raw material nor process of weaving is undertaken for manufacturing of non woven fabric.

The flow chart for manufacturing of non woven fabric

The Supreme Court in the case of M/s Porritts and Spencer (Asia) Ltd., on which the applicant has relied, had the occasion to discuss the term ‘textiles’. The Court observed:

“The word ‘textiles’ is derived from the Latin ‘texere’ which means ‘to weave’ and it means any woven fabric. When yam, whether cotton, silk, woollen, rayon, nylon or of any other description as made out of any other material is woven into a fabric, what comes into being is a ‘textile’ and it is known as such. It may be cotton textile, silk textile, woollen textile, rayon textile, nylon textile or any other kind of textile. The method of weaving adopted may be the warp and weft pattern as is generally the case in most of the textiles, or it may be any other process or technique. There is such phenomenal advance in science and technology, so wondrous i.e. the variety of fabrics manufactured from materials hitherto unknown or un-thought of and so many are the new techniques invented for making fabric out of yam that it would be most unwise to confine the weaving process to the warp and weft pattern. Whatever be the mode of weaving employed, woven fabric would be ‘textiles’. What is necessary is no more than weaving of yarn and weaving would mean binding or putting together by some process so as to form a fabric.”

The issue before the Court was whether ‘dryer felts’ fall within the category of “all varieties of cotton, woollen or silken textiles”. The Court held that dryer felts are, therefore, clearly woven fabrics and must be held to fall within the ordinary meaning of the word ‘textiles’. We do not think that the word ‘textiles’ has any narrower meaning in common parlance other than the ordinary meaning given in a dictionary, namely, a woven fabric.”

The judgment in the case of Delhi Cloth and General Mills Ltd. vs. State of Rajasthan and others relied upon by the applicant is distinguishable. The Supreme Court, in that case interpreted that the term ‘rayon fabrics’ falling in item 18 of the Schedule to the Rajasthan Sales Tax Act, 1954, also included ‘rayon tyre cord fabric’ manufactured by the petitioner. Entry51 of Schedule B appended to the HVAT Act uses the term ‘textile’.

In view of this interpretation of the term ‘textile’, the non woven fabric cannot be treated as ‘textile ‘. Entry 51 of Schedule B which exempts “All varieties of cotton, woollen or silken textiles including rayon, artificial silk or nylon” is restricted to textiles only. Therefore, non woven fabrics do not come within the ambit of entry 51 and are not exempted from levy of VAT. The product non woven fabrics do not fall in the list of Goods of Special Importance mentioned in Section 14 of the CST Act, 1956. The product is also not covered by any entry of any Schedule appended to the Act, therefore, is an unclassified item liable to tax @12.5% plus 5% surcharge.

The matter is clarified accordingly.

Signed by Sanjeev Kaushal, Additional Chief Secretary to Government, Haryana, Excise & Taxation Department (Chandigarh Dated the: 21.03.2017)